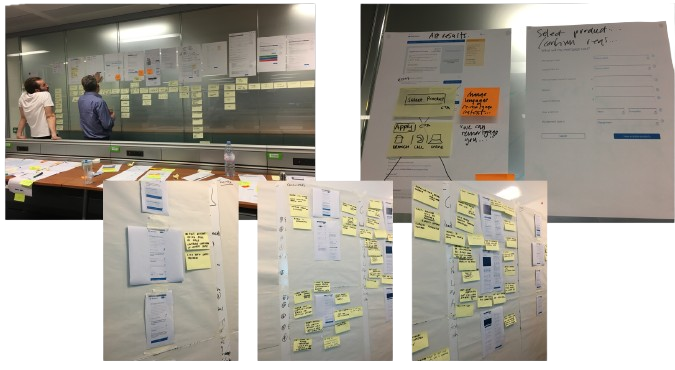

A thorough analysis of every screen in the journey provided valuable insights into user interactions, revealing pain points, friction areas, and opportunities for improvement. This process also played a key role in maintaining consistent branding, ensuring each screen felt cohesive and preventing user confusion caused by abrupt design or functionality changes.

" Don’t understand product

types and terms

(eg, early repayment)"

Amba

"Have I submitted the right documents?"

Isaac

"The bank does not treat me as a person."

Nga

"When I contact the bank, the person I talk to can’t help."

Steph